Moldmaking Industry Scrambles to Repurpose and Focus on the Battle Against COVID-19

The Moldmaking Index adjusts as the world economy pauses to address COVID-19.

.jpg;width=70;height=70;mode=crop;format=webp)

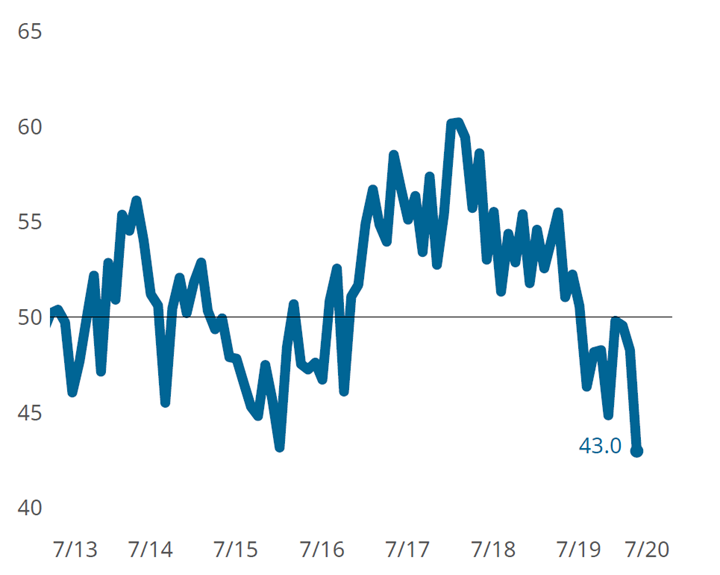

The GBI: Moldmaking fell 5 points in March registering 43.0. Gardner Intelligence’s review of the underlying index components observed that the Index — calculated as an average of its components — saw all-time lows set for new orders, exports and employment. It is important to remember that these readings represent the breadth of change occurring within the metalworking industry experiencing and are not to be understood as representing the rate of change. These low readings indicate only that a large proportion of metalworking manufacturers reported some decreased level of business activity without quantifying the magnitude of the downward change.

Moldmakers reported challenging conditions in March as the Index registered its second lowest reading in recorded history. All business activity components reported challenging conditions.

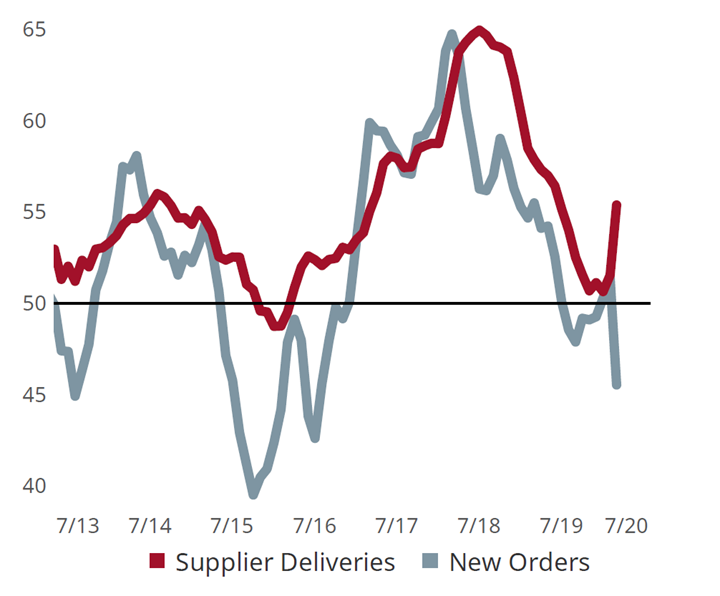

March’s data reported an unusual combination of events as the reading for supplier deliveries moved upward while those for all other components contracted sharply. The reason for this has to do with how the supplier delivery question is asked with the response options being ‘slower’, ‘same’ and ‘faster’. In normal times when demand for upstream goods is high, supply chains cannot keep pace with these orders. The resulting backlog of supplier orders thus lengthens their delivery times. This delay causes our surveyed firms to report slowing or lengthening delivery times which by our survey’s design reports that change as an increase in the supplier deliveries reading. The world’s efforts to slow the spread of coronavirus, or COVID-19, has significantly disrupted supply chains worldwide. It is thus due to this disruption, as opposed to strong demand for upstream products overall, that the supplier deliveries have lengthened and the reading has increased.

Survey respondents reported a steep contraction among most elements of business activity. The reading for supplier deliveries is designed to increase when supplier deliveries slow under the assumption that suppliers are experiencing higher backlogs and need longer to get parts to manufacturers. In the current situation, it is COVID-19’s massive disruption to the world’s supply chains that is causing longer delivery times.

The Moldmaking Index is unique in its ability to measure business conditions specific to the molding industry and to do so on a monthly basis. The challenges facing manufacturers today require leaders to have good data in order to make effective forward-looking decisions. It is thus particularly important at this time for our readers to complete the Moldmaking Index survey sent to them each month. Your participation will enable the best and most accurate reporting of the true impact that COVID-19 is having on the moldmaking and molding industry.

Related Content

-

Moldmaking GBI Returns to Contraction After One-Month Respite

After a challenging move into the 50s in March, the April GBI returned to a mostly consistent state of contraction, the result of recent market dynamics.

-

Moldmaking Sector Sees Future Optimism Despite Current Challenges Subhead

Strong future expectations signal potential rebound as automotive and medical sectors prepare for growth.

-

Moldmaking Activity Returns to Accelerated Contraction

February’s index dropped from the more positive readings seen in January, landing on par with July 2023 and remaining in contraction mode.